As banks tighten their lending criteria and borrowers look for faster access to capital, non-bank and private lenders are filling the gap. They’re funding a broad range of financing needs such as small business expansions, short-term property deals and equipment upgrades.

“Following the global financial crisis and the Banking Royal Commission, banks became subject to stricter capital adequacy requirements and more conservative lending practices,” explained Clare George, Associate Director Commercial at broking firm LMG, speaking at the recent National Equipment and Commercial Finance (ENCF) Forum.

“Private credit providers have stepped in, offering tailored loan structures, flexible repayment terms and faster execution times.”

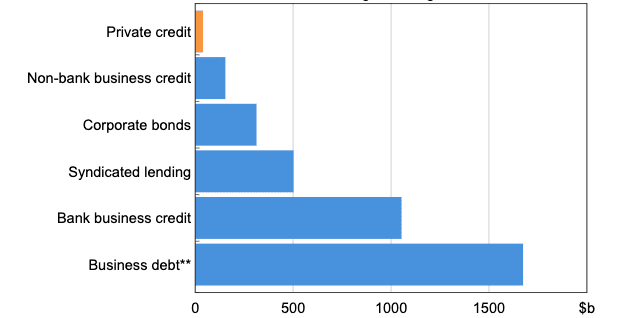

The Reserve Bank of Australia estimates the local private credit market at around $40 billion, or roughly 2.5% of total business debt. In comparison, non-bank commercial real estate lending alone was valued at $74 billion at the end of 2023 and is forecast to reach $146 billion by 2028.

Outstanding business lending as at August 2024*

* Lending to non-financial businesses.

** Business debt includes business credit, corporate bonds and other types of lending.

Source: Reserve Bank of Australia, Bulletin – October 2024

The growth of non-banks and private credit has created new funding channels for small and medium businesses as well as property developers who might otherwise struggle to get finance. For investors, these markets offer diversification and often stronger returns than many traditional options.

Distinctly different models

While both non-bank and private lenders offer alternatives to banks, they operate through very different models.

Non-banks are institutional in nature. “They’re regulated, have formal credit policies and often resemble banks in their operations,” said Jean-Pierre Gortan, Managing Director of Simplicity Loans & Advisory, at the ENCF Forum.

Non-bank lenders, for example, hold Australian credit licences and must comply with responsible lending laws. They raise capital through securitisation or wholesale funding.

On the other hand, private lenders are often high-net-worth individuals or boutique funds that use their own capital or pooled money from investors. These providers can approve loans within hours and negotiate terms on a case-by-case basis.

Notably, not all of them hold an Australian credit licence.

“They’re less regulated, more nimble and often priced for risk,” added Gortan. “That flexibility is an advantage, but it demands more caution.”

Likewise, loans negotiated via these lenders may fall outside the National Consumer Credit Protection Act 2009 (Cth) when structured as business credit. Without the consumer safeguards and formal governance of non-bank lenders, brokers and borrowers are responsible for conducting due diligence.

“Brokers need to understand the true nature and purpose of the loan, not just the legal structure,” said George.

Balancing flexibility and risk

Many brokers now turn to private lending solutions to meet their clients’ needs, such as non-conforming loans and funding gaps for property transactions, according to Anja Pannek, Chief Executive of Mortgage & Finance Association of Australia (MFAA).

“As traditional lenders pull back due to regulatory and economic pressures, demand for credit hasn’t gone away, and that’s where the flexibility of private lending is proving its value,” she said at the ENCF Forum.

But flexibility comes with risk. The MFAA has warned that many private lenders operate with limited oversight, which recently prompted the Australian Securities and Investments Commission (ASIC) to step up its scrutiny. Earlier this year, ASIC released a discussion paper on the rise of private credit and followed that with a series of actions against non-compliant lenders.

This has placed greater responsibility on brokers. The ENCF Forum advises checking a lender’s track record, Australian Financial Complaints Authority (AFCA) membership, dispute processes, funding stability and documentation. It also recommends making sure clients understand the total cost, including fees and conditions.

“Education is key,” said George. “Brokers must go beyond the surface, ask the right questions, and never assume a loan structured as business credit removes consumer protections.”

Sorting the legitimate from the risky

According to Shore Financial broker Tom Bracey, private lending “has become so big that it’s under the eye of AFCA. You can pretty much determine who’s legit and who’s not these days just by doing some simple due diligence.”

But pitfalls remain. Bracey said he has seen cases where private lenders failed to honour funding terms, although reputable ones refunded application fees.

He advised borrowers to work with experienced brokers who know which lenders to avoid.

“One of the key things that you’ll find is these guys who say they’ve got the money and they don’t have the money. They’ll ask you for a massive upfront fee as a working fee,” added Bracey.

“Speak to a broker who knows development finance, that’s a start.”

{kind=link}